Private sector debt in New Zealand stood at $456bn in March 2019, the equivalent of almost $92,000 for each of our 4,957,400 men, women and children. This article explores the key contributors to this debt, as well as basic rules of thumb to put this debt in context.

New Zealand’s debt can be broadly split in three types:

- household debt

- business debt

- agricultural debt

These three debt types accounted for approximately 98% of all private debt in New Zealand. We will explore each of these debt types in turn.

Household debt accounts for 60% of private sector debt

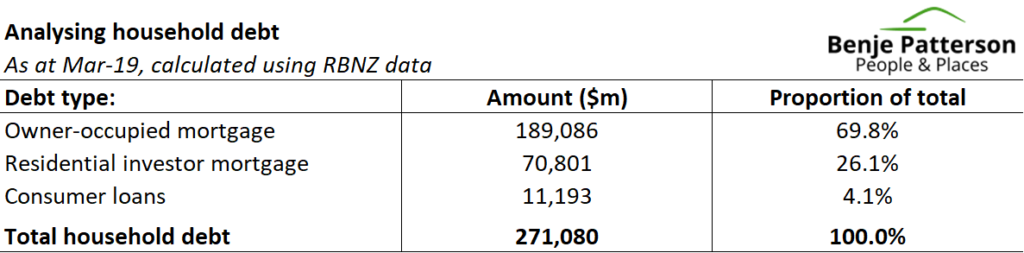

Household debt is the largest contributor to private sector debt, accounting for 60% ($271bn) of the total.

The following table breaks this household debt into its parts.

Most of the household debt is in the form of residential mortgages, spread across mortgages to owner-occupiers (70%) and residential investors (26%). Only a small proportion of debt (4.1%) is in the form of consumer loans (like personal loans and credit cards).

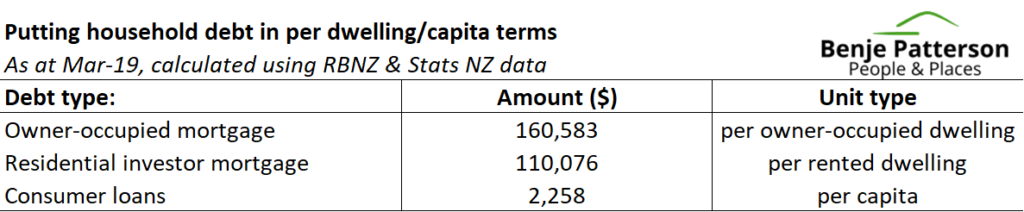

The average mortgage is $160,583

Much can also be learned from considering household debt in per dwelling or per capita terms.

The following table shows that the total value of outstanding mortgages to owner-occupiers is equivalent to a $160,583 mortgage for each owner-occupied dwelling in New Zealand. By comparison, the total value of outstanding mortgages to residential investors is equivalent to just $110,076 per rented dwelling. This finding flies against the commonly-held view that most rented residential properties are controlled by highly leveraged investors.

At first brush, mortgage debt appears relatively low compared to average house prices of approximately $687,000 (as at March 2019). However, one needs to bear in mind that the distribution of debt is what matters for considering how risky it is for financial stability. In its May 2017 Financial Stability Report, the Reserve Bank of New Zealand (RBNZ) found that 19% of households, who had taken out a new mortgage, had debt levels that exceeded 5 times their income. Only 6% of existing borrowers, on the other hand, had that same level of indebtedness.

Turning to consumer debt, the table shows that consumer debt is just $2,258 per capita. In per household terms, this consumer debt represents the equivalent of $6,345 per household. Compared to mortgage debt, these consumer loan amounts may appear low. However, remember that consumer debt is often higher interest bearing and not usually secured directly against assets that hold their value, such as a property.

Business debt accounts for 24% of private sector debt

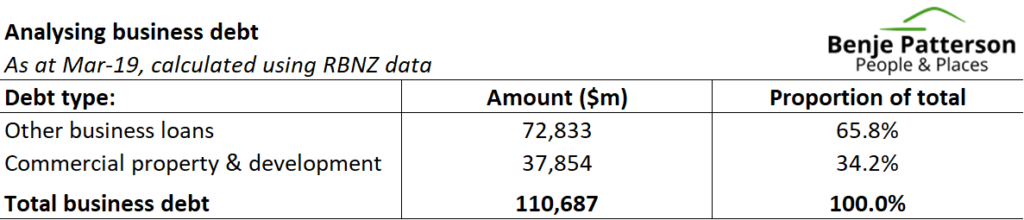

Business debt is the second largest contributor to private sector debt, accounting for 24% ($111bn) of the total.

The following table breaks this business debt into its parts.

Most business debt is on assorted business loans (66%) for things like plant and machinery, or as a source of credit for working capital. Commercial property loans account for 34% of business debt and are used to finance both investment in commercial property and its development.

Business profits are ample to service debt

Much can also be learned from considering business debt on a per business basis.

Business Demography data from February 2018 shows that there were 534,933 businesses in operation in New Zealand, with 169,686 of these businesses operating in the construction, development or real estate space.

Using these statistics on business units highlights that each business in New Zealand carried an average of $136,153 of assorted business loans, while there were $223,083 of commercial property and development loans outstanding for every business operating in that space.

Relative to revenue and profits, the $111bn of outstanding business loans appear to be at a manageable level. Statistics NZ’s Annual Enterprise Survey shows that total business revenue in 2018 was $691.9bn ($1.3m per business), while total business profits were $85.6bn ($160,020 per business).

Agricultural debt accounts for 14% of private sector debt

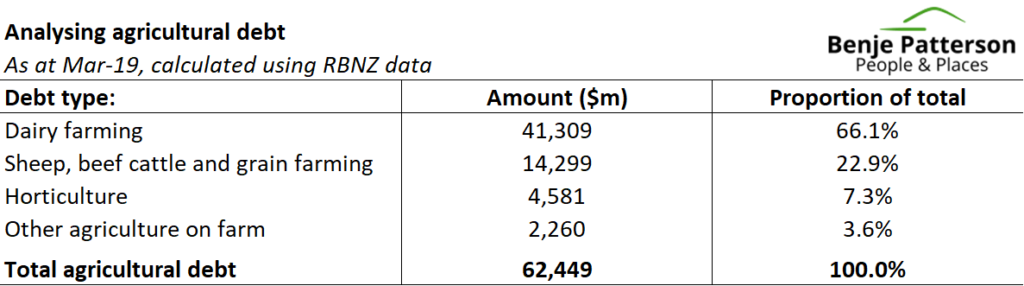

Agricultural debt is the third largest contributor to private sector debt, accounting for 14% ($62bn) of the total.

The following table breaks this agricultural debt into its parts.

Approximately two thirds of all agricultural debt is carried by the dairy sector, while sheep and beef farmers accounted for 23% of debt. The next biggest contributor is horticulture (7.3% of debt).

Dairy debt high compared to farm values

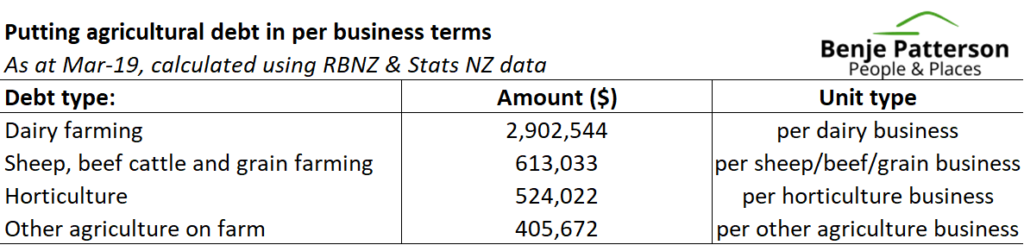

It is once again useful to put this debt on a per business basis.

The following table displays agricultural debt on a per business basis using business unit data for each type of agriculture taken from Statistics NZ’s Business Demography framework.

The data shows that the average dairy farm carries just shy of $3m of debt. Given that Dairy NZ reported the average dairy farm to be about 144 hectares, this debt can also be expressed as approximately $20,000 per hectare. This debt level sits quite high compared with an average sale price of dairy farms of about $25,000 per hectare in June. Previous Dairy NZ surveys have suggested that approximately two thirds of a typical dairy farm’s assets were tied up in land/buildings.

Other parts of the agricultural sector carry a much lower level of debt per business unit.

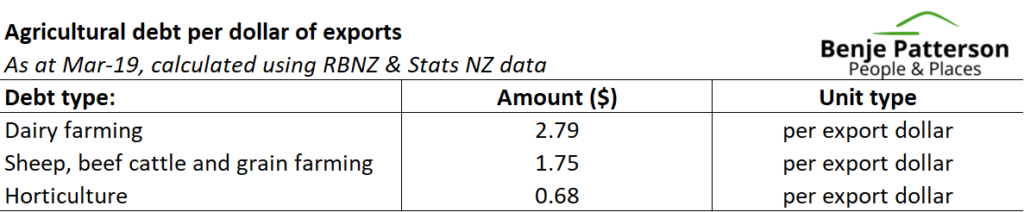

Dairy debt also high compared to exports

Another way to express business debt is by comparing the debt to export earnings to get an indication of how much debt it takes to generate $1 of exports.

The following table shows debt of the dairy, sheep/beef and horticulture sectors against export receipts for each sector. Other agriculture is not covered due to data limitations.

The data again clearly shows that the dairy sector has a much higher level of indebtedness than its peers in sheep and beef, and in horticulture. There was $2.79 of dairy debt carried for every $1 earned in dairy exports during the March 2019 year. By comparison, the horticulture sector carried just 68 cents of debt for every $1 of export earnings.

Concluding remarks

This article gave some basic metrics for understanding which parts of New Zealand are most indebted, and what that debt means for each household and business.

Following the indebtedness of key parts of the economy is important for understanding the balance of financial risks we face.

Debt itself is not inherently bad – we need to borrow from time-to-time to smooth cash flows and invest in assets. We do need to be careful though that the debt we take on is used in productive ways over the long-run.

Debt is something we should talk more about as a country. The challenge though is that much of the data on debt provided by organisations such as the Reserve Bank is not in a format accessible to many.